The State Pension: What to expect

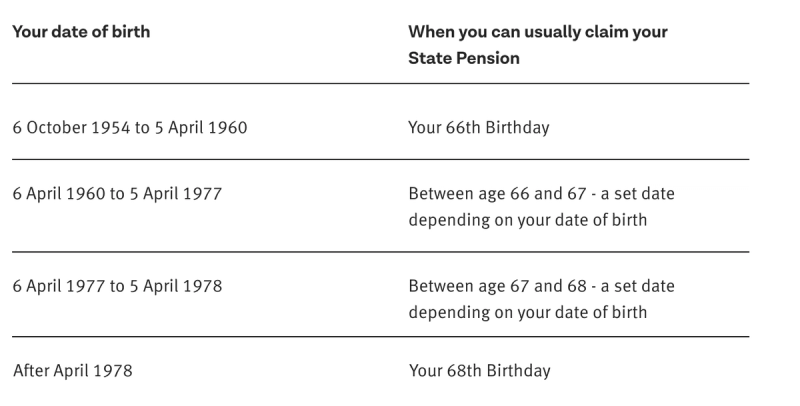

The State Pension is an important part of your retirement income. It’s provided by the government and is based on your National Insurance (NI) contributions. If you’re born after 6 April 1978, you are currently able to access your pension from age 68, although this could change in the future.

You’ll need 35 years’ worth of contributions for the full State Pension. The current full State Pension is: £230.25 per week (or £12,014.12 per year)

You can check your personal forecast through the UK Government website. This will tell you:

- How much you’re likely to receive.

- When you’ll get it.

- How to increase your pension if needed.

The State Pension is a regular payment from the government to people who have reached a certain age and have made enough National Insurance (NI) contributions. Here are some of the main points to understand about the UK state pension:

1. Eligibility

To qualify for the State Pension, you generally need at least:

- 10 years of qualifying NI contributions to get the minimum (currently £65.79 a week)

- 35 years of qualifying NI contributions to get the full amount (currently £230.25 a week)

- If you have between 11 and 34 years, you’ll receive a proportion of the full State Pension.

Qualifying NI contributions are normally made:

- when you’re working and made NI contributions, or you earned more than the lower earnings limit per year (currently £6,500 per year)

- using National Insurance credits if you’ve received certain benefits such as Child Benefit or Jobseeker’s Allowance

- paying voluntary NI contributions (link: www.gov.uk/voluntary-national-insurance-contributions)

2. Age Requirements

The current state pension age is gradually increasing and varies depending on your date of birth. It's currently 66 for both men and women, but this is set to rise to 67 by 2028, with potential further increases later.

3. The State Pension

New State Pension: Applies if you reached state pension age on or after April 6, 2016, and the amount depends on your NI record, with a maximum currently around £230.25 per week (for 2025-2026).

4. How It’s Paid

- Payments are typically made every four weeks, directly into a bank or building society account.

5. Additional Benefits

- The State Pension is independent of other benefits; however, some people may qualify for other support (e.g., Pension Credit) if their State Pension income is low.

- People can also get additional NI credits if they’re eligible for certain benefits or have gaps in their NI record.

6. Deferral Options

- You can delay taking your state pension. For each year you defer, you could receive a higher weekly amount later.

7. Tax Implications

- The state pension is taxable income, so if your total income exceeds your personal allowance, you may have to pay tax on it. The State Pension is paid gross, which means it’s paid to you without the deduction of Income Tax. HM Revenue & Customs will adjust your tax code to take into consideration the amount of State Pension being paid. If you owe Income Tax, it will usually be paid by your workplace pension or employment income (if applicable).

8. Impact of Workplace/Private Pensions

- The state pension can be received alongside workplace and private pensions, and you can work while receiving it.